The aftermath of the COVID-19 crisis, plus solid housing demographics, has created a genuine problem with housing inventory. Record low inventory has resulted in a hectic housing market with forced bidding becoming typical rather than the exception.

One of my biggest concerns for the U.S. housing market from 2020 to 2024 is that price growth could push higher than we had seen in the previous decade. In February of 2020, housing demand started to pick up. This was a real breakout in demand due to improved demographics for home buying, but because we received this data in March when we were in the throes of the COVID-19 crisis, no one seemed to notice.

The social and fear-driven shutdowns caused a freeze in purchasing activity. Still, after a few weeks, housing market demand trumped COVID-19 fears, and housing had an epic V-shaped recovery in purchase applications. The rest is history.

However, this hot housing market is not accompanied by a credit boom because the actual number of sales is up only slightly. The raw shortage of homes on the market is why buyers face multiple-bid situations for any home.

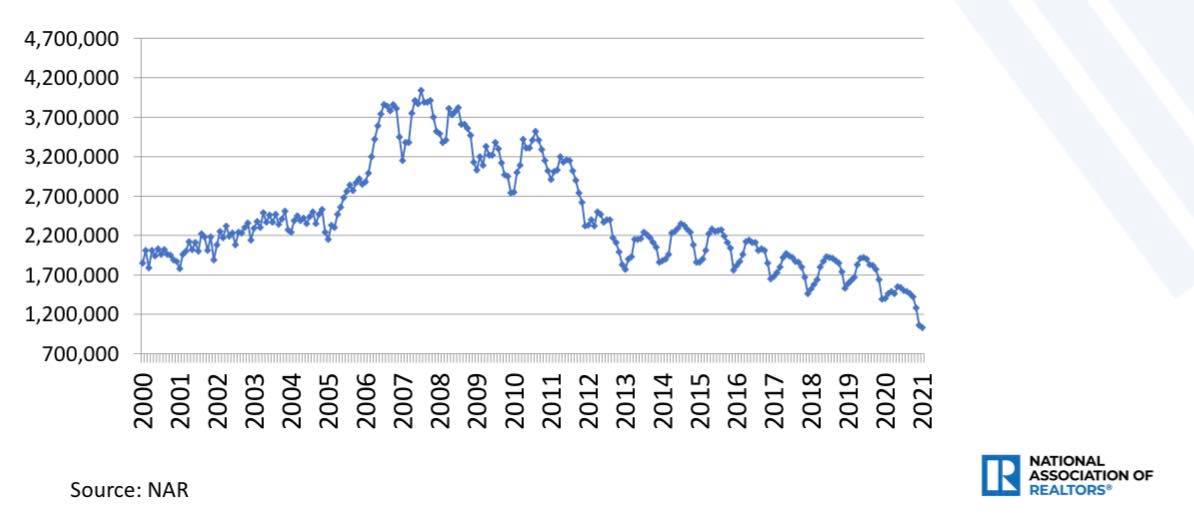

This downtrend in inventory started in 2014, and not even 5% mortgage rates budged the data too much higher.

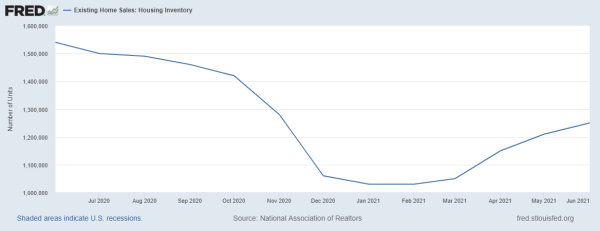

On a positive note, total inventory has been rising since February. This is the typical seasonal shift that occurs every year, and as such, the home-price growth rate should be cooling down in terms of speed of growth. Some of the housing prices data lag, so we should see it in the upcoming months. However, this isn’t saying a lot since home price growth has gone parabolic like a lot of pricing data.

However, total inventory is still below levels that I would consider consistent with a healthy market, where buyers choose homes and don’t need to overbid. If we could get inventory between 1.52 and 1.93 million, although still historically low, the bidding war madness would disappear, and the days on the market should grow.

I don’t want to see inventory fade as we move into fall and winter, as it typically does, then stay at this low base for 2022. Also, be careful in reading into percentage increases from this record low. It might seem like inventory levels are growing, but they’re not in big, significant terms. This is why I emphasized the total inventory levels of 1.52 – 1.93 million as promising targets for us to root for.

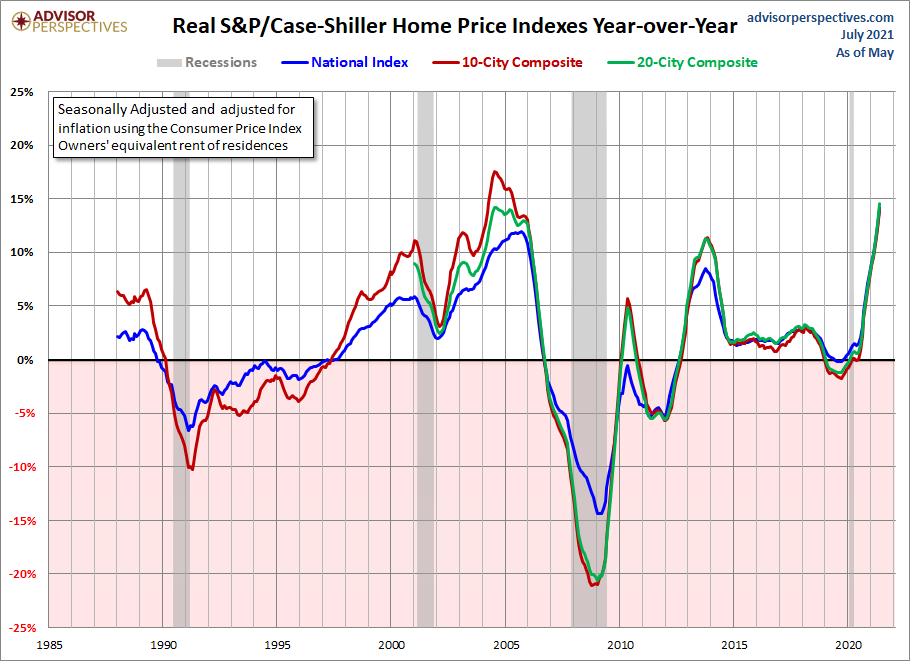

In 2019, we briefly had negative real home price growth, which I wrote was very healthy for the housing market. I would love to see three years of that type of action, but wanting something and having it happen are two different things.

With the summer seasonal uptick in inventory, we should see the growth rate of home prices cool in the coming months. This isn’t much comfort for buyers still looking to purchase because home prices have gone vertical since 2020. I hope we get a repeat of what happened in 2013-2014, which was the last time we saw price growth skyrocket then cool down in 2014.

But it is a much different housing market today than in 2014. Demographics are better now. Most importantly, mortgage rates have not gone up. In 2014, mortgage rates getting over 4% was key to cooling home price growth.

In August 2020, I wrote that what could cool down the market is that the 10-year yield would go over 1.94%. — but I didn’t expect that to happen in 2021. For my 2021 forecast, I capped my 10-year yield range at 1.94%. Currently, the 10-year is at 1.36%, with a peak yield of around 1.75%. The bond market has stayed within the scope of 0.62% to 1.94%, with the main channel being the range of 1.33% to 1.60% needed to be created in 2021.

Home prices are not going to get much help from mortgage rates in 2021. Good demographics mean demand will be stable for the existing home sales market. Sales appear to be doing a tad better than I expected. I anticipated more existing home sales prints to be under 5,840,000 — and so far, that is the case for only one print.

Remember, 2020 total existing-home sales ended at 5,640,000 and, so far, every print this year has been higher. Even if we get some prints under 5,840,000 for the rest of the year, we will still end 2021 with pre-cycle highs in demand for the existing home sales market.

For the remainder of the year, keep an eye on inventory levels. If we can hold the gains in inventory and have inventory rise next year, we get the balance in the market that we are hoping for, along with an end of the bidding wars. The current market of 2020-2021 is demonstrating that people can still afford to buy homes with mortgages. More Americans bought houses with mortgages in 2020-2021 than in any other period from 2008-2019.

This goes to show you that mother demographics is a powerful force. We can add the move up, move down, and cash buyers and investors for the existing home sales market. It is tough to get the velocity of inventory to grow when demand is stable.

Even in 2014, when purchase applications were trending down 20% year over year, and sales went negative year over year, inventory levels moved higher, although not by much.

After 2014, we started the long eight-year road to where we are today. While people were screaming about a second housing crash, years 2020 and 2021 proved that untrained professional grifters trying to sell fear got their &^%$ handed back to them by mother demographics and the United States of America.

It is important to remember that the existing home sales and new home sales markets are very different. Supply for the new home sales market has spiked to over 6.5 months, two times since 2018. For the existing home sales market, that hasn’t happened once — even in 2014.

Inventory for the new home sales market is essentially back to where it was in the previous expansion. If inventory for new sales goes over 6.5 months, on a three-month average, builders take notice and back off new construction.

Our take-home for today is to keep an eye on the seasonality factor for inventory. If we see inventory fade into the fall and winter, that isn’t positive.

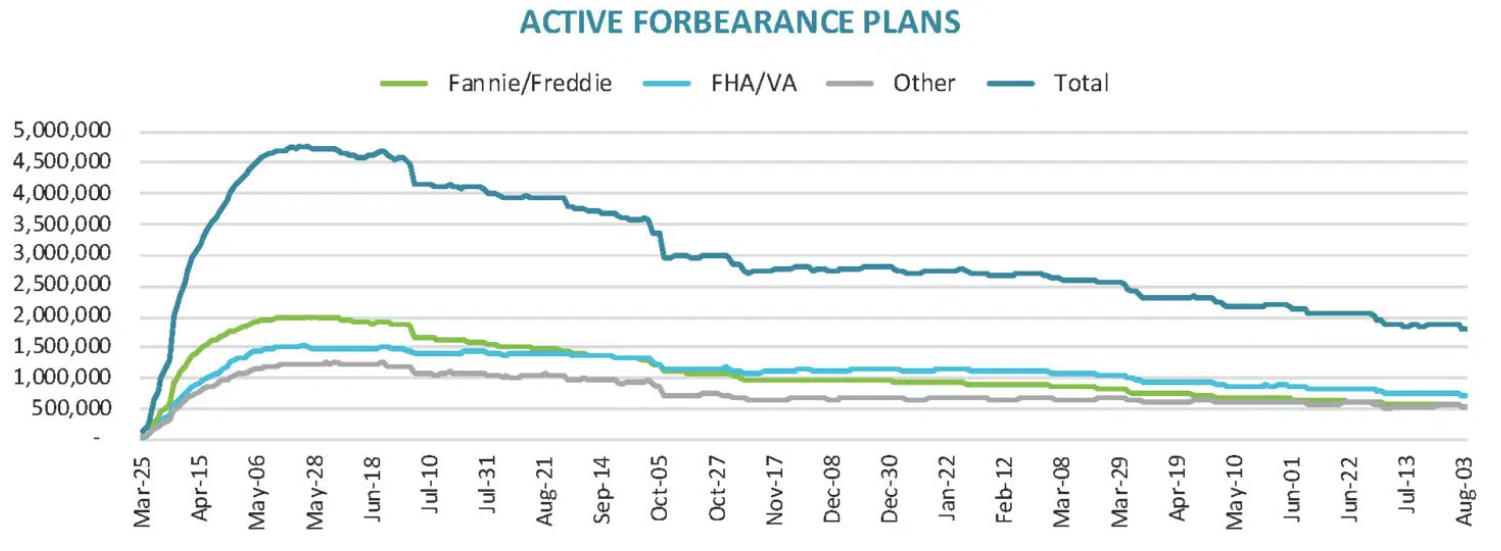

Regarding loans in forbearance, I don’t see this as a problem lying in wait for the housing market like what we saw in 2008. Nothing about this recent housing market reminds me of 2008, outside the hot pricing.

The number of loans in forbearance has gone from near 5 million to 1.74 million. From Black Knight:

While I believe we will see some increase in inventory when this program expires, as I explained here, It might not be as much as I thought for 2021; time will tell here. The desire for those who are primary resident owners, not investment homeowners, to stay in their homes with the jobs coming back was the baseline premise of why I never believed in what the forbearance crash bros were selling last year and this year.

We are 5.7 million jobs away from getting back all the jobs lost due to COVID-19. I still believe we will get all those jobs back by September 2022 or earlier. The delta variant can delay some things for sure, but this America is Back recovery train took off in April of 2020 and isn’t looking back. The bulk of the jobs that haven’t come back are in three sectors:

- Lesuire and Hospitality (1,740,000 lost)

- Education and Health Service (950,000 lost)

- Government (780,000 lost)

- Service sector (4,990,000 jobs lost)

- Goods-producing sector (710,000 jobs lost)

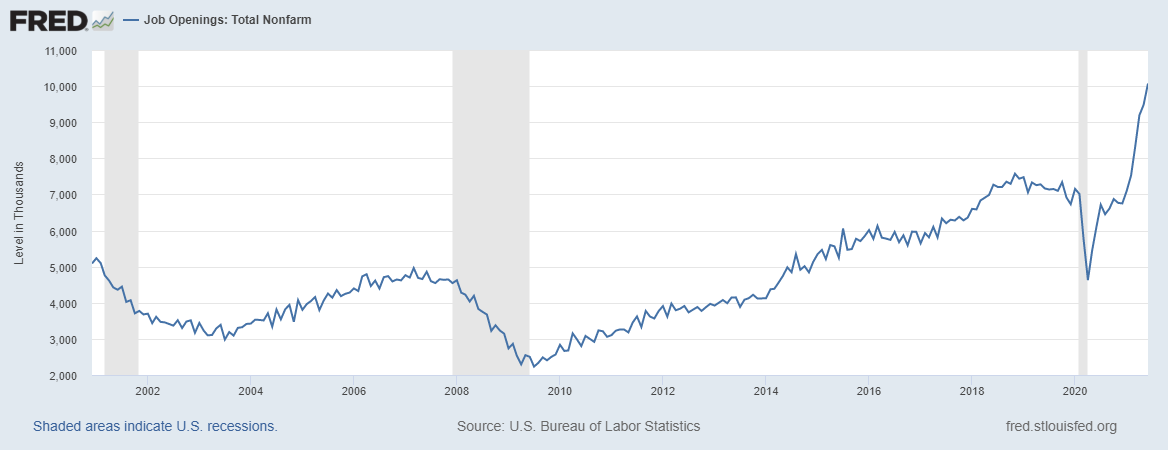

We have a lot of open positions waiting to be filled. We will get there. For many months, I have been talking about job openings hitting 10 million, and we just got that print this week.

This year is not like 2008 when jobs openings were around 2 million and we lost nearly 8.8 million jobs in the great financial crisis. Today we have 5.7 million jobs left to gain and over 10 million job openings. Forbearance will be under 1 million at some point next year, and the GSEs’ delinquencies will be under 1%. This is great news for America and our people — but terrible news for our woebegotten housing bubble boys and the forbearance crash boys. Alas.

However, for those of us who want to see much more inventory stick, seasonality and forbearance might not give us what we want to see in 2021. This is something to keep an eye on the rest of the year as inventory rising and sticking higher is the No. 1 thing I want to see in this housing market.